The Future of Credit Unions: What the House of Commons Report Means for Real People

The future of banking is digital, community-focused, and accessible to everyone

In July 2025, The House of Commons published a comprehensive report on credit unions revealing significant insights into the sector's future direction. For those unfamiliar with credit unions or questioning their relevance, this report outlines developments that could fundamentally transform how millions of people access financial services.

Understanding Credit Unions

With origins dating back to the 1850s, Credit unions represent a community-focused alternative to traditional banking. They operate as member-owned cooperatives, prioritising financial inclusion over profit maximisation. The key distinction is that members who deposit funds also hold ownership stakes and voting rights in the organisation's governance.

However, UK credit unions operate under a "common bond" membership requirement. This means potential members must share specific connections with existing members - whether through geographical location, employment, occupation, or organisational affiliation. This creates an exclusive membership model, similar to a professional association, but for financial services.

The Numbers Tell a Story

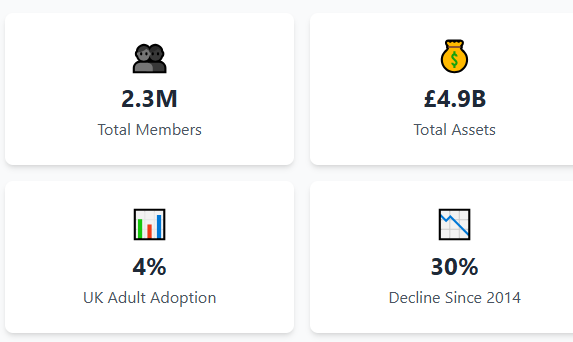

The House of Commons report shows some interesting trends. Right now, there are about 2.3 million people using credit unions across the UK, which sounds like a large number until you realise that it is only 4% of adults. Compare that to Ireland where they have over 4 million members in a much smaller country.

The number of credit unions is shrinking (down 30% since 2014), but the ones that are left are growing in assets and serving more people. It's similar to what happened when many small corner shops closed, but the remaining ones became small supermarket chains.

Current Operational Challenges

From manual processes to automated solutions - the transformation credit unions need

The report identifies several critical challenges facing the credit union sector:

Legacy Systems and Manual Processes: Many credit unions continue to rely on outdated operational methods. Loan applications and compliance verification require manual processing and as a result, administrative tasks consume disproportionate resources. This creates significant inefficiencies compared to digitally-enabled competitors.

Financial Sustainability Concerns: Operating costs are increasing faster than revenue growth. The report shows expenses rose by 4.86% while income grew by only 1.40% in the previous year. This trend threatens long-term viability without operational improvements.

Regulatory Compliance Burden: Financial services regulations continue to expand in complexity. Credit unions must implement comprehensive Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures, along with extensive compliance reporting. For smaller organisations with limited resources, these requirements represent substantial operational challenges.

Demographic Engagement Issues: The current member base skews towards older demographics. Younger consumers expect mobile-first experiences, instant approvals, and sophisticated digital interfaces. Traditional credit unions struggle to compete with modern fintech applications that offer seamless user experiences.

What's Coming Next?

The future of finance: combining digital convenience with community care

To help credit unions grow and compete better the government is planning some pretty significant changes

Bigger Service Areas

Under existing legislation, as a result of the common bond of geography rule, a new credit union can only cover a maximum of 3 million potential members meaning, for example, that it wouldn't be possible to operate a credit union for all Londoners. The government wants to remove this cap so credit unions can serve larger areas and more people.

Better Family Access

Currently, only people in your household can join the credit union where you're a member. The government wants to expand this to include family members, so your children could join even if they don't live at home anymore.

Shared Services

Small credit unions struggle because they can't afford up-to-date technology or compliance systems. The government wants to make it easier for them to share the costs of improved systems through what they call a Credit Union Service Organisations (CUSOs).

Northern Ireland Catch-Up

Credit unions in Northern Ireland have been operating under older, more restrictive rules. They're planning to bring their laws up to date with the rest of the UK.

The Technology Solution

This is where technology partners like Madiston become strategically important. The Commons report essentially outlines a roadmap for digital transformation that aligns precisely with Madiston's platform capabilities.

The sector requires several key technological capabilities:

- Automated loan processing systems (delivered through Madiston's platform)

- Real-time compliance verification (integrated KYC/AML automation)

- Mobile-first member experiences (comprehensive digital interface)

- Cost-effective shared technology platforms (Madiston's core business model)

The timing represents a significant market opportunity for Madiston and other providers. While government reforms are removing regulatory barriers to credit union growth, technology providers like Madiston are developing the infrastructure necessary to capitalise on these legislative changes.

Why This Matters for Regular People

Credit unions are often thought of as just for people for whom high street banks are unwilling to open a bank account. They're now becoming a legitimate alternative for anyone who wants:

- Better Rates: Because they're not trying to maximise profits for shareholders, credit unions often offer better interest rates on savings and cheaper loans.

- Personal Service: You're not just an account number. Credit unions actually care about their members' financial wellbeing.

- Community Focus: Your money stays local and helps people in your community rather than disappearing into a nationally operating financial company hence leaving the community that provided the money.

- Democratic Control: You get a vote in how your credit union is run. If your money is in a high street bank, you certainly won't.

The Irish Example

The report mentions that Ireland has the highest credit union membership in the world outside the Caribbean. In Ireland, credit unions are mainstream - not just for people who can't access traditional banking. They've managed to modernise while keeping their community focus.

If the UK government's proposed changes are implemented, we could see something similar happening here. Imagine credit unions that are as easy to use as digital banks but with the personal touch and community benefits that big banks can't match.

Challenges Ahead

It won't all be smooth sailing though. The report identifies some real risks:

Cybersecurity: As credit unions go digital, they become targets for hackers. They need proper security measures, not just hopes and prayers.

Competition: FinTech companies and digital banks are moving fast. Credit unions need to catch up quickly or risk becoming irrelevant.

Governance: Many credit unions are run by volunteers who might not understand modern technology or digital risks. They need proper training and support.

What Happens Next?

The government is consulting on these changes right now, which means they're asking for feedback before making final decisions. If you're involved with a credit union or thinking about joining one, this is actually a good time to have your say.The consultation can be found on the Bank of England site:

The changes they are proposing could make credit unions much more competitive and accessible. Combined with better technology from companies like Madiston, we could be looking at a real renaissance for the credit union movement.

Looking Forward

Credit unions have historically focused on community-based mutual support. The House of Commons report demonstrates government recognition of this value proposition and commitment to supporting sector modernisation. With appropriate technology partnerships and regulatory reforms, credit unions could reclaim significant market share in UK financial services.

For consumers, these developments promise increased choice, competitive rates, and financial services that prioritise community benefit over shareholder returns. In an increasingly corporate banking environment, this represents a meaningful alternative.

The future of financial services need not be dominated exclusively by large corporations or impersonal digital platforms. The optimal model may combine credit unions' community focus with modern technological convenience. If current government proposals succeed, this vision may become reality sooner than anticipated.

To learn more about how digital transformation can modernise your credit union operations while preserving community values, contact Madiston to see how their automated lending platform is supporting financial institutions in their digital transformation journey.

Author: Abubakar Sadiq Babalele

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.