5 minutes reading time

(936 words)

Open Finance - coming to banks, fintechs, corporates and you!

Author: Professor Brian Scott-Quinn.

You may not be aware of this but it is a fact that Volkswagen AG has been looking at scenarios in which it no longer has more than a niche place in the automative world! Why else would it have decided to put €1bn into a small car manufacturer with a commitment to increase this to €5bn - and even more so when this car manufacturer has never made a profit and was on the verge of possible bankruptcy??

The reason is very simple. VW has not been able to develop its own electric vehicle software to the standard, quality, user experience (UX) and versatility of that which Chinese car manufacturers now offer. The most worrisome Chinese car companies from VWs point of view are BYD and NEO. If VW is in danger of extinction, think how many other companies, and not just car companies but in other industries which are not keeping up with the current revolution in IT/AI are at risk.

The risks are similar in financial services. Open Finance is going to mean either in-house building of new systems to cope with the changes necessary to meet regulatory requirements or buying in systems which are already "Open Finance" ready. In addition, Open Finance is likely to make the big banks potentially more competitive with fintechs and make some fintechs uncompetitive.

To explain what we have stated above, the company which VW is investing in is a US electric auto manufacturing company called Rivian - a company that most people in Europe will not have heard of. It is a start-up founded in 2009 but it has found "scaling-up" production difficult and costly. It is very good at developing "the software defined vehicle" which is the way today's electric car market is moving but not so good at scaling-up the metal bashing side of manufacture. On the other hand, VW is good at metal bashing but not so good at software. So its potentially a great fit of two good companies which should help both. Rivian will produce the software for both companies while VW will help Rivian with scaling-up 'metal bashing'.

Open data permissioning and regulation (Open Finance) is likely to turn the financial sector upside-down just as electrification of the economy, in particular road vehicles, is turning the automotive and other sectors upside-down. In banking we had the Payments Services Directive 2 (PSD2) in 2019 which was intended to make it easier for new payments operators (fintechs) to compete with the large banks. Now the European Commission is introducing PSD3 along with Financial Data Access (FIDA) which could, in contrast to PSD2, help the big banks more than the smaller fintechs unless they take anticipatory action. It's not just in the European Union that we will see this development. With the new UK government anxious to keep our regulatory frameworks in line with those in the EU, its coming to us soon.

At present, banks are forced to provide current account information to potential competitors with no reciprocity by fintechs. Once in force (2025/26) the data-sharing ecosystem will be available equally to both sides of the fence. Thus the banks will be able to access a lot more relevant financial information about potential borrowers (subject to the potential borrower agreeing access) via APIs than before. Equally fintechs will be able to do so as well, of course if their platforms are set up to achieve this. But the previous competitive advantage that fintechs have in this respect had will be gone - forever.

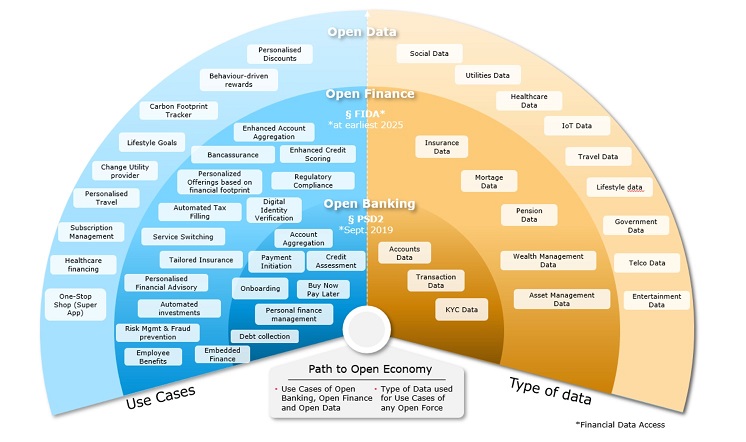

We use the expression "Open Finance" but technically, this is an outcome of FIDA. In the graphic below from Eraneos , a Swiss and German consultancy, we can see where we are at present (the inner core which is Open Banking), and where we are moving to by 2025/6 which is Open Finance. The outer ring is Open Data, something that does not exist at present but it is likely that some countries will move in this direction also.

On the left of the diagram in blue we have the possible uses that data availability has made possible and will increasingly make more use cases possible. In the inner core we have Open Banking which improved credit assessment for non-banks as well as the other use cases indicated. Open Finance could enable more effective credit assessment as it would be able to interrogate other financial aspects of a potential borrower's life (subject to permission from the potential borrower). But of course banks would now also have the same ability to access other relevant financial institution data which is a huge advance from the banking industry's point of view compared with PSD2. On the outer circle we have what could be possible in future with Open Data but that looks a little too much like the type of information that the Chinese government likes to record on all its citizens.

The reason is very simple. VW has not been able to develop its own electric vehicle software to the standard, quality, user experience (UX) and versatility of that which Chinese car manufacturers now offer. The most worrisome Chinese car companies from VWs point of view are BYD and NEO. If VW is in danger of extinction, think how many other companies, and not just car companies but in other industries which are not keeping up with the current revolution in IT/AI are at risk.

The risks are similar in financial services. Open Finance is going to mean either in-house building of new systems to cope with the changes necessary to meet regulatory requirements or buying in systems which are already "Open Finance" ready. In addition, Open Finance is likely to make the big banks potentially more competitive with fintechs and make some fintechs uncompetitive.

To explain what we have stated above, the company which VW is investing in is a US electric auto manufacturing company called Rivian - a company that most people in Europe will not have heard of. It is a start-up founded in 2009 but it has found "scaling-up" production difficult and costly. It is very good at developing "the software defined vehicle" which is the way today's electric car market is moving but not so good at scaling-up the metal bashing side of manufacture. On the other hand, VW is good at metal bashing but not so good at software. So its potentially a great fit of two good companies which should help both. Rivian will produce the software for both companies while VW will help Rivian with scaling-up 'metal bashing'.

Open data permissioning and regulation (Open Finance) is likely to turn the financial sector upside-down just as electrification of the economy, in particular road vehicles, is turning the automotive and other sectors upside-down. In banking we had the Payments Services Directive 2 (PSD2) in 2019 which was intended to make it easier for new payments operators (fintechs) to compete with the large banks. Now the European Commission is introducing PSD3 along with Financial Data Access (FIDA) which could, in contrast to PSD2, help the big banks more than the smaller fintechs unless they take anticipatory action. It's not just in the European Union that we will see this development. With the new UK government anxious to keep our regulatory frameworks in line with those in the EU, its coming to us soon.

At present, banks are forced to provide current account information to potential competitors with no reciprocity by fintechs. Once in force (2025/26) the data-sharing ecosystem will be available equally to both sides of the fence. Thus the banks will be able to access a lot more relevant financial information about potential borrowers (subject to the potential borrower agreeing access) via APIs than before. Equally fintechs will be able to do so as well, of course if their platforms are set up to achieve this. But the previous competitive advantage that fintechs have in this respect had will be gone - forever.

We use the expression "Open Finance" but technically, this is an outcome of FIDA. In the graphic below from Eraneos , a Swiss and German consultancy, we can see where we are at present (the inner core which is Open Banking), and where we are moving to by 2025/6 which is Open Finance. The outer ring is Open Data, something that does not exist at present but it is likely that some countries will move in this direction also.

On the left of the diagram in blue we have the possible uses that data availability has made possible and will increasingly make more use cases possible. In the inner core we have Open Banking which improved credit assessment for non-banks as well as the other use cases indicated. Open Finance could enable more effective credit assessment as it would be able to interrogate other financial aspects of a potential borrower's life (subject to permission from the potential borrower). But of course banks would now also have the same ability to access other relevant financial institution data which is a huge advance from the banking industry's point of view compared with PSD2. On the outer circle we have what could be possible in future with Open Data but that looks a little too much like the type of information that the Chinese government likes to record on all its citizens.

Source: Swiss and German consultancy, Eraneos.

We have considered the European Union framework for Open Finance. But, as we noted above, a comparable framework is coming soon to the UK also and to several other countries. The question is who will be ready for it? Open Banking relied mostly just on APIs. This next transition will also depend on banks and fintechs mastering data management, AI and machine learning. It's a whole new world. But those platforms, such as from Madiston PLC, which is planning for this exciting new future, will enable their customers to take advantage of Open Finance as soon as it is launched.

Stay Informed

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.